Related Post: What if CPF minimum sum continues to increase at its current rate

Some readers may be still confused on how the minimum sum works. Some of the queries they have may include:

1) If my CPF OA + SA is more than 131k, does it mean that I can withdraw all balances above the 131k at the age of 55?

2) If I do not hit the minimum sum, can I withdraw anything?

I have extracted some of the examples provided on the CPF website

(Examples on computation of CPF withdrawal)

I will go through the examples in the reverse order as I feel it is easier to understand in this manner.

Example 4: CPF balances more than $145,556

1) fulfilled his CPF minimum sum

2) fulfilled his medisave required amount

In this scenario, X will be able to withdraw all cash balances above his 131k OA+SA (250,000 - 131,000 = 119,000). You will fall into this category if your CPF balances are more than $145,556. But wait!! Isn't the CPF minimum sum $131,000. Where did this new number come from?

Extracted from CPF website:

For this group: More than $145,556

10% of $145,556 and any further cash balances after setting aside the CPF Minimum Sum (MS) of $131,000** (from July 2011 to June 2012) and the prevailing Medisave Required Amount ($32,000 for 2012)

My calculations:

10% of 145,556 (14556) + 131,000 = $145,556

The 131,000 only forms 90% of the $145,556. So "10% of $145,556 and any further cash balances after setting aside the CPF Minimum Sum (MS) of $131,000" can be read as "All balances above $131,000" if you belong to this category. Confusing isn't?

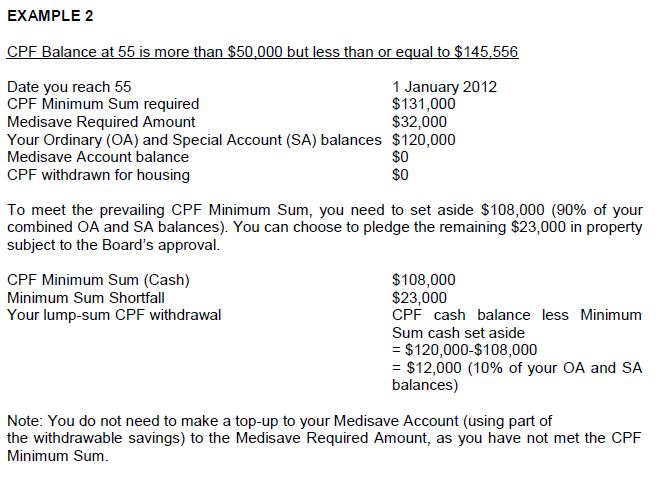

If you fall between the 131,000 to 145,556 region, you need to refer to example 2

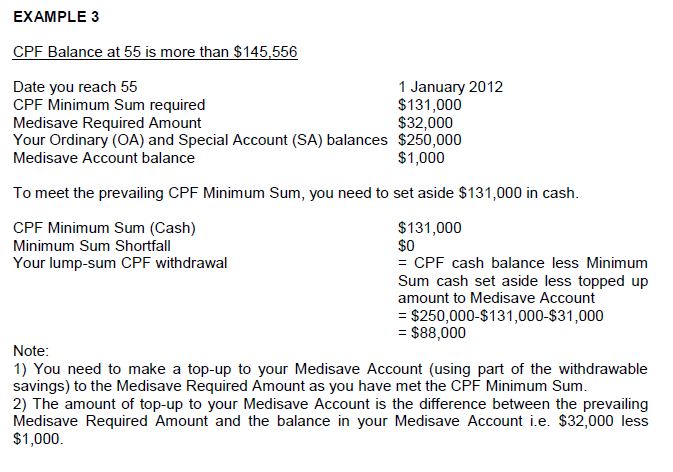

Example 3: CPF balances more than $145,556, but medisave requirement not fulfiled

1) fulfilled his CPF minimum sum but

2) did not fulfill his medisave required amount

In such a scenario, he will need to top up his medisave from his OA + SA 1st before withdrawing the balances. In the example above, we see that his medisave has a shortfall of 31k to achieve the required amount. This 31k needs to be topped up from his OA+SA. X ended up only withdrawing 88k.

Example 2: More than $50,000 but less than or equal to $145,556

Things start to get tricky from here.

1) did not fulfill his CPF minimum sum

2) did not fulfil his medisave required amount.

Does it means that he cannot withdraw anything? Not at all.

For this category, he can withdraw "10% of the cash balances. The remainder will be set aside in your RA.".

If you belong to this category, do take note of the following:

1) You do not need to top up to your Medisave account as you have not met the CPF minimum sum. (good news isn't? You can withdraw more now)

2) You can choose to pledge the remaining amount using your property.

In a scenario where X has 140k and has fulfilled the Medisave required amount, he will be able to withdraw 10% (i.e. 14k). This is slightly more than the 9k (140k - 131k) which I originally thought to be!

Example 1: More than $5,000 but less than or equal to $50,000

In this example, after withdrawing 5k, X has 3k remaining. In addition to this, X chose to pledge his property (addtional 30k that was withdrawn for housing earlier)

What if your minimum sum is below $5,000 ?

In such a scenario, you will be able to withdraw all your cash balances. =)

Final Notes

I hope most of you will eventually end up in the scenario where you hit the CPF minimum sum and Medisave required amount. This will ensure that you can get a bigger payout from your CPF LIFE later on. But as I have mentioned before, it will be better to plan your retirement without taking CPF into consideration. We never know how the CPF withdraw rules or the CPF LIFE scheme may change over the next few years.

No comments:

Post a Comment